The first thing to notice is simple. CBAM is no longer a future issue. It entered its definitive phase on 1 January 2026, and customs systems now validate authorisations before goods are released for free circulation. That makes compliance a border issue, not just a reporting issue.

For importers, CBAM penalties are now tied to real operational risk. The older transitional period ended at the close of 2025, when reporting still happened without a financial adjustment. From 2026 onward, the rules changed shape, and the pressure became much more direct.

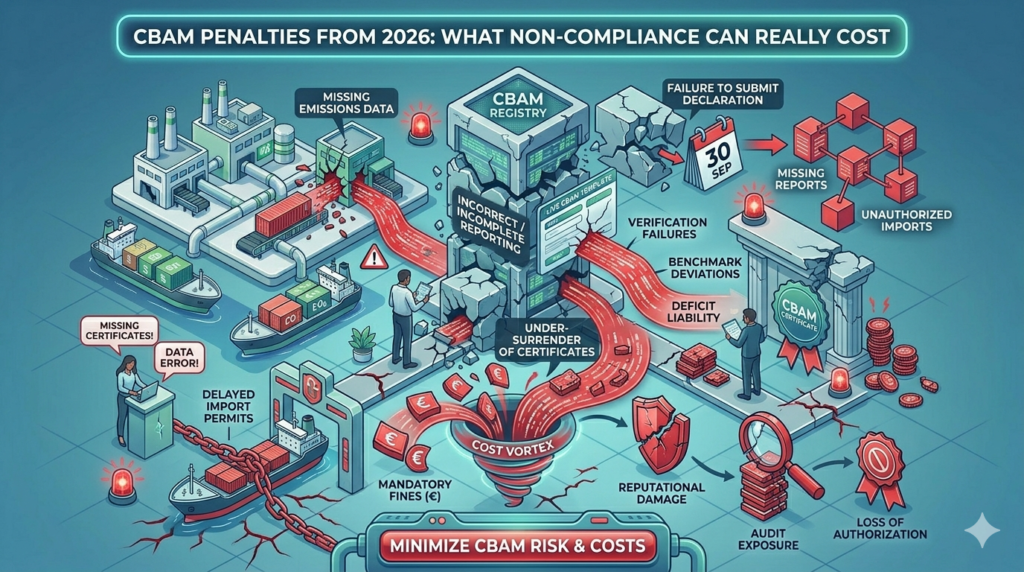

What changed on 1 January 2026

From the start of 2026, CBAM became part of the definitive regime. The European Commission says customs authorities validate CBAM authorisations before release for free circulation, and that validation is linked with the 50-tonne threshold now being monitored at the border level. In plain terms, paperwork alone is no longer enough. The import side now depends on formal authorisation.

That change matters because CBAM non-compliance is no longer limited to a late report or a missed filing window. The system now reaches into customs clearance itself. If the importer is not an authorised CBAM declarant, the goods may simply not move as expected.

What counts as non-compliance

The official CBAM FAQ explains that, during the transitional period, missing, incorrect, or incomplete CBAM reports could trigger a correction procedure. If the reporting declarant failed to take the necessary steps to correct the report, the national competent authority could apply penalties. That framework shows how seriously the EU treats data quality, even before the financial phase fully begins.

From 2026, the stakes are higher. The regulation says customs authorities shall not allow importation of goods by any person other than an authorised CBAM declarant. That means non-compliance can include more than a wrong number on a form. It can include importing without the right status, failing to secure authorisation, or failing to meet the new definitive obligations.

A practical way to think about CBAM penalties is this. One layer is administrative, and another layer is operational. A company may face sanctions for poor reporting. A company may also face import problems if the authorization side is ignored. That combination makes the regime stricter than a simple filing rule.

What the penalties look like

During the transitional period, the Commission’s FAQ states that reporting declarants may face penalties ranging between EUR 10 and EUR 50 per tonne of unreported emissions. That is the clearest official numerical range available from the Commission’s guidance on the reporting phase.

For the definitive phase, the picture is tougher. A Council document from 2025 says that, where an authorised CBAM declarant or an importer fails to comply, penalties will be applied and the amount will be based on penalties in the EU ETS. The same document also says that, in repeated offences, the national competent authority may decide to suspend the declarant’s account.

That is an important shift for CBAM non-compliance. The regime is no longer only about correcting emissions data after the fact. It is moving toward stronger enforcement, closer to the logic used in EU ETS rules. In other words, repeated mistakes may stop looking like clerical issues and start looking like systemic risk.

Why this matters for businesses

The obvious risk is money. The less obvious risk is delay. If authorisation is missing, customs clearance may stall. If data is incomplete, corrections may be required. If the same mistakes keep happening, authorities may treat the case more harshly. That is where small gaps become expensive.

This is why CBAM penalties should be read as more than fines. They also represent lost time, blocked shipments, and extra administrative pressure. For companies that run tight supply chains, even a short delay can ripple outward very quickly.

A useful mental model is this. CBAM is not just checking whether emissions exist. It is checking whether the importer can prove them, submit them, and manage them through the right channel. That is a much wider obligation, and it raises the cost of sloppy compliance.

How to reduce the risk

A few habits can make a real difference.

- Check whether authorisation is already in place.

- Keep emissions records complete and consistent.

- Review supplier data before submission.

- Correct errors as soon as possible.

- Treat customs status as part of compliance.

These steps may sound basic, but they reduce the chance of CBAM non-compliance becoming a border problem. That matters because the system now links reporting, authorisation, and clearance more tightly than before.

The bigger picture

CBAM was designed to prevent carbon leakage and bring imported goods closer to the carbon cost faced inside the EU. The definitive phase, which began on 1 January 2026, makes that idea much more concrete. It is now built into customs operations, reporting duties, and sanctioning logic.

So the real lesson is fairly plain. CBAM penalties are not a side issue anymore. They are part of the business model for import compliance. Companies that treat CBAM as a one-time paperwork task may run into problems fast. Companies that treat it as a live operational obligation are likely to handle it better.

And that is probably the safest reading of the current rules. January 2026 did not just begin a new reporting year. It marked the point where CBAM enforcement became much more immediate, much more connected to customs, and much less forgiving.

FAQs

What are the main CBAM penalties from 2026?

The definitive phase brings stronger enforcement, customs-based authorisation checks, and penalties that are based on EU ETS principles. The Commission also says customs will not allow imports by anyone other than an authorised CBAM declarant.

Does CBAM non-compliance only mean late reporting?

No. It can also mean missing authorisation, incomplete reporting, incorrect reporting, or failure to correct errors after a correction procedure begins.

What was the penalty range during the transitional phase?

The Commission’s FAQ states that penalties could range from EUR 10 to EUR 50 per tonne of unreported emissions. That figure applies to the reporting phase guidance.

Can customs stop the import of CBAM goods?

Yes. The Commission’s guidance says customs authorities shall not allow importation by anyone other than an authorised CBAM declarant. The Commission also says authorisation is validated before release for free circulation.

Can repeated violations lead to harsher action?

Yes. A Council document says repeated offences may lead the national competent authority to suspend the declarant’s account. That makes repeated CBAM penalties exposure much more serious.